Carmignac Portfolio Merger Arbitrage Plus: Letter from the Fund Managers

Dear Investors,

During the last quarter of the year, our Carmignac Merger Arbitrage (I share class EUR Acc) achieved a performance of 1%, while Carmignac Merger Arbitrage Plus (I share class EUR Acc) rose 1.1%.

In the last quarter, M&A activity showed a real rebound compared with the previous quarter. Indeed, 86 M&A deals announced in the US, Europe and Asia during Q4 2023 were eligible for our portfolio, which was up 32% on the previous quarter. As usual, the US remains the largest market with 48% of the total, with Europe and Asia sharing the remainder with 26% and 27% each. The average deal size is $6 billion in the US, compared with around $2 billion in Europe and Asia. When we look at M&A activity by value, the upturn is even more notable, with a total of $340 billion worth of deals announced in the last quarter, almost double the figure for the previous quarter.

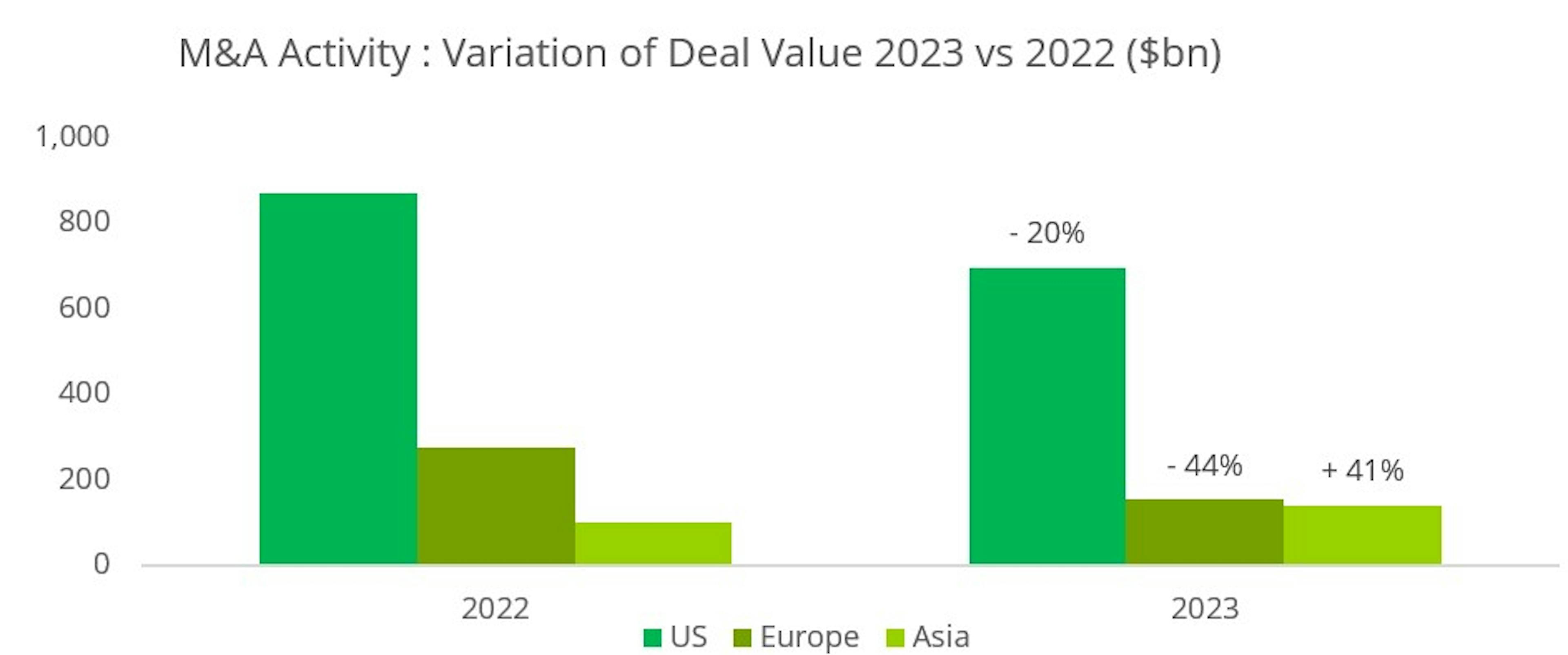

The final quarter is also a good time to take stock of the M&A year that has just ended. At the start of the year, many thought that rising interest rates in the US and Europe would bring M&A activity to a halt. While it is true that there has been a decline in value this year, a detailed analysis reveals a more complex reality. In fact, M&A activity has decreased overall in value in 2023 compared with 2022: deals announced during this year represented a total of $991bn, an annual decline of 20%. There are several points to bear in mind when analysing this figure.

Firstly, this fall is actually smaller than one might have feared at the start of the year, given the scale and speed of the rise in interest rates.

Secondly, the level of activity achieved this year is in line with what was seen on average before 2018, when rates were significantly lower. The geographical disparity is also interesting to note: while the US is down by 20%, Europe is down more sharply by 44%, while Asia is up by 41%.

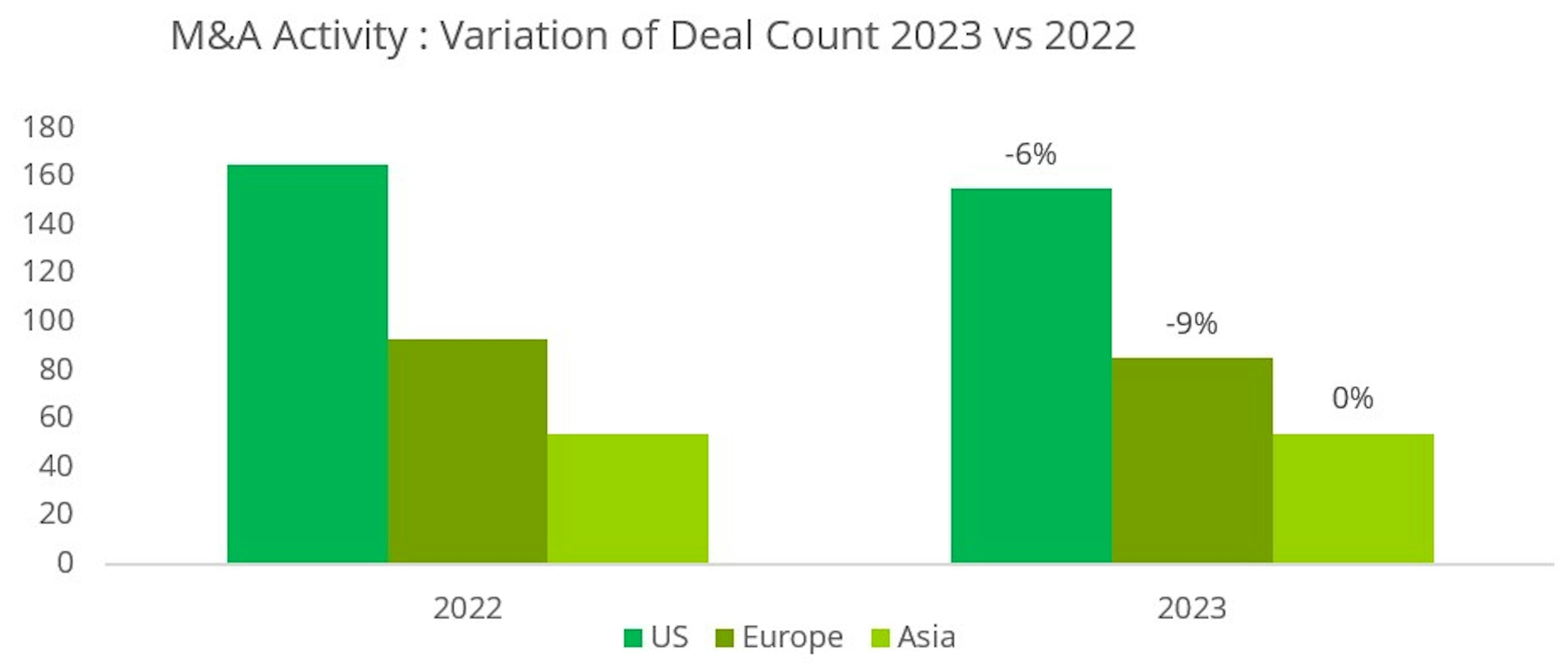

Finally, if we look not at value but at volume, i.e. the number of transactions, the fall in M&A activity is much more modest. With 294 new deals announced for 2023, the fall is only 6% on 2022.

This is an important point to emphasise because, for us as arbitrageurs, it is the number of transactions, rather than the size of the deals themselves, that enables us to deploy capital in our funds while maintaining good diversification.

The sectoral breakdown of M&A activity is also interesting to analyse, as it reflects a real change from what we have seen in the recent past, and probably foreshadows a new trend for the future.

We are witnessing the return of the "old economy". While Healthcare and Technology remain two important sectors, accounting for 20% and 11% respectively of total announced deals in the US, Energy has become the leading sector with 26% and Industrials/Commodities the third with 14%. In Asia, the trend is even more pronounced, with the Industrial/Raw Materials and Utilities sectors together accounting for almost 70% of the total. The drivers behind this trend are powerful and structural: sector growth driven by the energy transition, a solid balance sheet for strategic players, and significant synergies and economies of scale in the event of mergers.

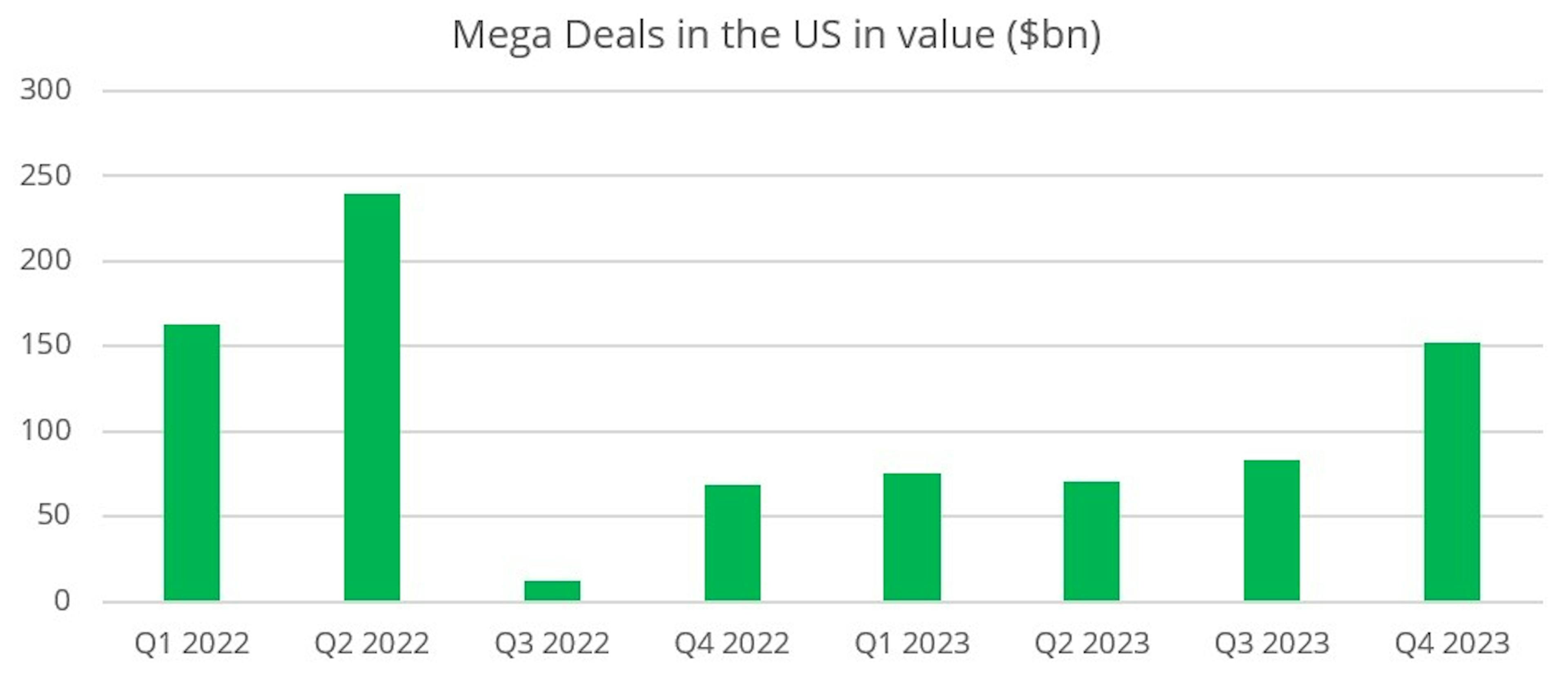

The final highlight of the year is the gradual return of "mega deals" in the US, i.e. deals in excess of $10bn, which had disappeared from the landscape somewhat during 2022. This type of deal had become the Federal Trade Commission’s (FTC) favourite target, particularly in key sectors such as technology (Activision, VMWare, Black Knight) and healthcare (Seagen). But the fact that the FTC failed to block some of these emblematic deals, such as Activision and Seagen, has probably given companies renewed confidence to embark on major external growth projects.

With the fall in the US 10-year yield and the prospect of the end of the cycle of key rate hikes, the equity and bond markets rebounded strongly in the last quarter of 2023, with the S&P 500 and US Investment Grade up 11.7% and 10.0% respectively.

Looking at the Merger Arbitrage strategy, our Carmignac Merger Arbitrage (I share class EUR Acc) and Carmignac Merger Arbitrage Plus (I share class EUR Acc) funds posted a more modest increase of 1% and 1.1% respectively, but which remains entirely satisfactory in terms of management objectives. Several factors explain this performance.

Firstly, the pressure from the anti-trust authorities, which we had seen at the start of the year, particularly in the USA, tended to normalise throughout 2023. Two major deals, Pfizer's $41bn takeover of Seagen and Cisco's $28bn acquisition of Splunk, were approved by the FTC during the fourth quarter.

We also benefited from two improved offers. The first was the result of the stock market battle to buy the management company Sculptor Capital between Rithm Capital and a group of investors led by Boaz Weinstein. Rithm Capital's initial offer was eventually increased by almost 14%. The second improved offer concerns the mining company Azure Minerals. Sociedad Quimica y Minera de Chile, a leading Chilean lithium miner, initially launched a standalone offer at AU$3.50, which was subsequently increased by almost 6% with the support of Australian company Hancock Prospecting.

Finally, a large number of transactions, 88 in total in the US, came to an end during the quarter. The convergence of discounts on these deals was a good performance driver at the end of the year.

On the other hand, several factors had a negative impact on the fund's performance during the quarter. While the FTC approved a number of major deals, it also launched in-depth investigations into two other transactions, Tapestry's acquisition of Capri Holdings in the luxury handbag sector and Campbell Soup's acquisition of Sovo in the food sector. Although partly anticipated by the market, this bad news led to a widening of the two discounts, creating greater volatility.

The other negative factor of the month was the high volatility of discounts in the oil sector, particularly the one on the Hess/Chevron deal. Tensions between Venezuela and Guyana escalated in December over the territorial dispute centred on the Essequibo region. After holding a referendum on Venezuelan sovereignty over the Essequibo, Venezuela launched a defensive military manoeuvre on the border between the two countries. As Hess holds the vast majority of its assets in Guyana, the discount on the deal initially fell sharply before tightening at the end of the month following a meeting between the Venezuelan and Guyanese heads of state mediated by Brazil. We note that the merger agreement between Hess and Chevron is extremely strong and that the escalation of tensions alone cannot be a sufficient reason to withdraw from this operation. Chevron has also reaffirmed its interest in acquiring Hess.

Finally, despite significant improvements, Brookfield and EIG Global Energy's bid for Australian power producer Origin Energy failed as a result of shareholder opposition led by the Australian Super pension fund. As we had correctly estimated the Origin Energy share price in the event of the deal failing, the impact on performance was limited.

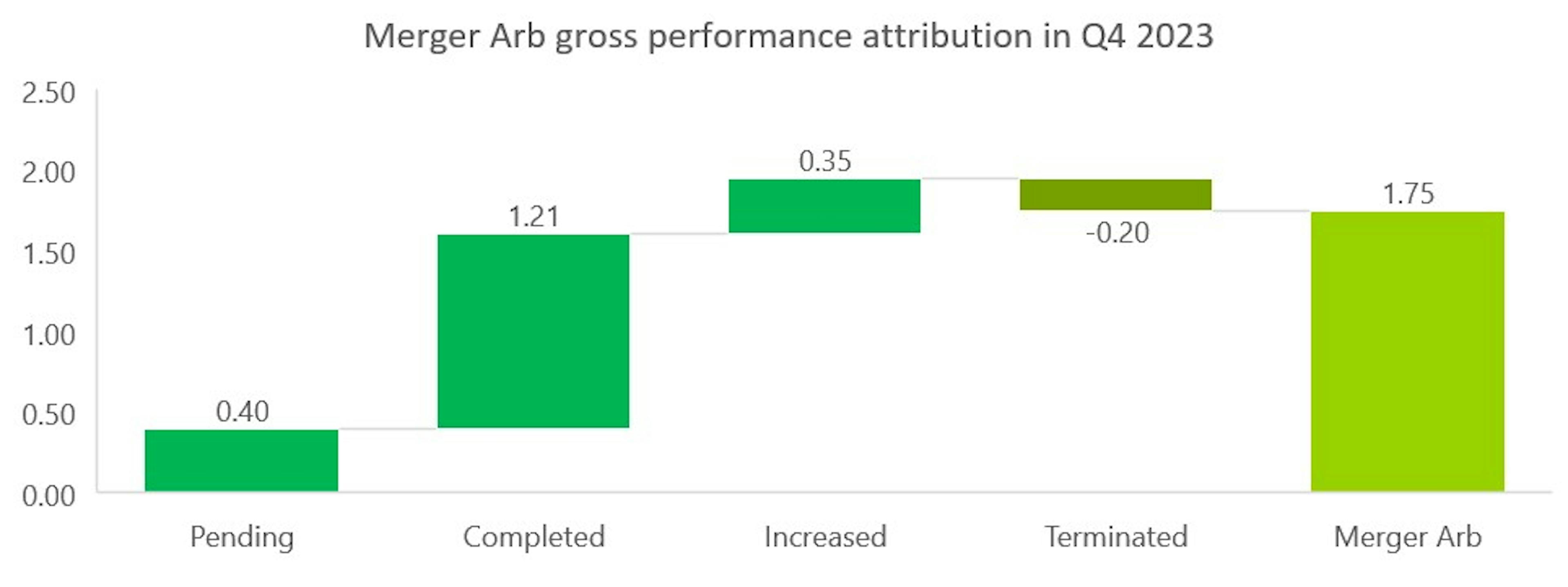

Another way of breaking down the fund's performance is to look at the status of the deal at the end of the period. A bid can be either:

- In progress: the deal has not yet been finalised because all the conditions precedent have not yet been lifted;

- Closed: the transaction has been finalised in accordance with the initial terms;

- Improved: the buyer has increased its price or a third party has come in with a higher offer;

- Abandoned: the deal failed.

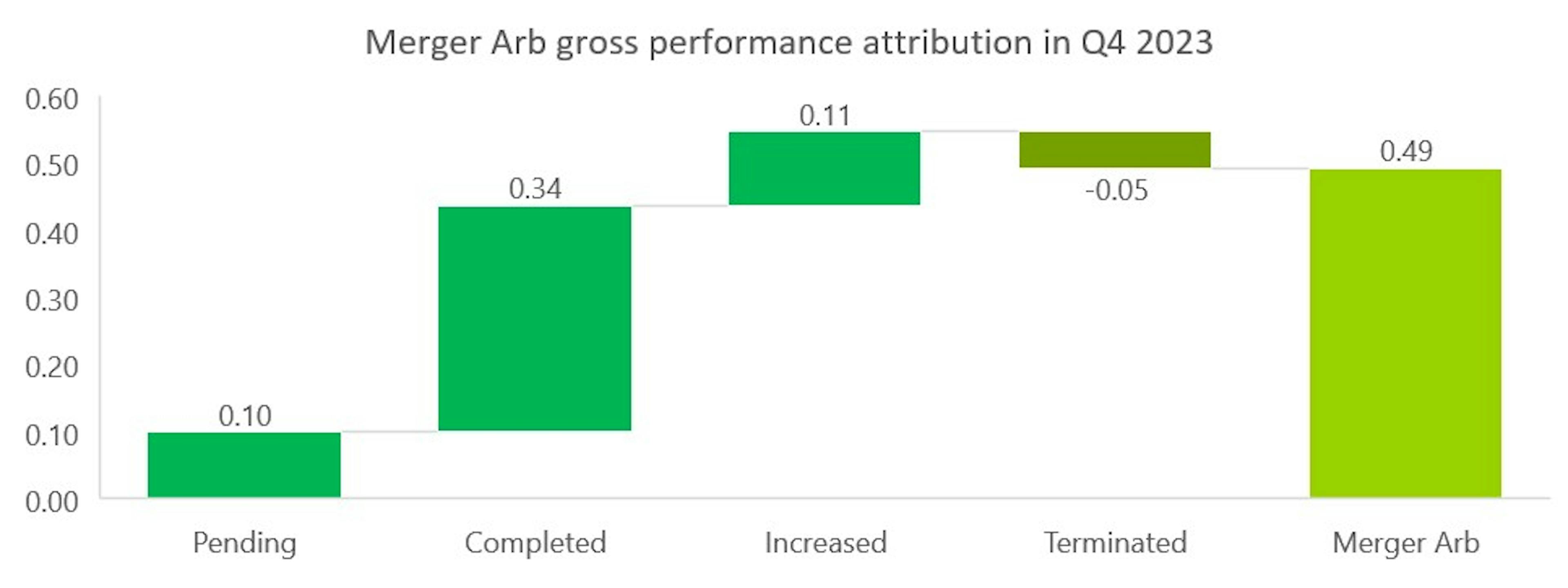

Using this methodology, we obtain the following performance attribution table for Carmignac Portfolio Merger Arbitrage Plus:

The table for Carmignac Portfolio Merger Arbitrage is as follows:

The main driver of performance was the completion of a large number of transactions in the portfolio. Given the increased volatility on certain discounts such as Sovo, Capri and Hess, the 'Pending' category contributed little to performance during the quarter. It should also be noted that the failure of the Origin Energy deal was more than offset by improved offers, notably the one for Sculptor.

This year-end is also an opportunity to take stock, since the funds were created in April 2023, of the two other key management parameters: volatility and correlation with the main asset classes.

In a year that was ultimately turbulent for all markets, our Merger Arbitrage strategy delivered on its promise of controlled volatility and low correlation. Carmignac Portfolio Merger Arbitrage has a volatility of 0.7% and a correlation to equities of 0.24 and High Yield credit of 0.12.

Carmignac Portfolio Merger Arbitrage Plus has a volatility of 2.1% and a correlation to equities of 0.26 and to High Yield credit of 0.14.

For the year ahead, we are confident that the good momentum seen in Q4 2023 will continue. Indeed, a historical study of M&A activity shows that, while there is a degree of cyclicality, downturns in activity tend on average to be short-lived. For 2024, the drivers of the recovery are already there:

- The end of the rate hike cycle is approaching, which should give business leaders a degree of visibility;

- Return of mega deals in most economic sectors;

- Sectoral shift in M&A activity towards the "old economy", driven in particular by the energy transition;

- A greater proportion of strategic players than financial players, who are more penalised by high interest rates;

- In some sectors, such as technology and healthcare, external growth is structurally an integral part of development models.

The Merger Arbitrage Team

Carmignac Portfolio Merger Arbitrage Plus

An active absolute return strategy focusing on merger arbitrage opportunitiesCarmignac Portfolio Merger Arbitrage Plus I EUR Acc

- Horizonte de investimento mínimo recomendado

- 3 anos

- Escala de Risco*

- 3/7

- Classificação SFDR**

- Artigo 8

*Escala de Risco do KID (documentos de informação fundamental). O risco 1 não significa um investimento isento de risco. Este indicador pode variar ao longo do tempo. **O Regulamento SFDR (Sustainable Finance Disclosure Regulation) 2019/2088 é um regulamento europeu que exige aos gestores de ativos que classifiquem os seus fundos como, entre outros: «Artigo 8» que promovem as características ambientais e sociais, «Artigo 9» que fazem investimentos sustentáveis com objetivos mensuráveis, ou «Artigo 6» que não têm necessariamente um objetivo de sustentabilidade. Para mais informações, visite: https://eur-lex.europa.eu/eli/reg/2019/2088/oj?locale=pt.

Principais riscos do fundo

Ações: O Fundo pode ser afetado por variações nos preços das ações, numa escala que depende de fatores externos,

volumes de negociação de ações ou capitalização bolsista.

Comissões

- Custos de entrada

- Não cobramos uma comissão de subscrição.

- Custos de saída

- Não cobramos uma comissão de saída para este produto.

- Comissões de gestão e outros custos administrativos ou operacionais

- 1,11% O impacto dos custos que suportamos anualmente pela gestão dos seus investimentos e outras comissões administrativas. Esta é uma estimativa baseada nos custos efetivos ao longo do último ano.

- Comissões de rendimento

- 20,00% como máximo da performance superior, se a performance for positiva e o valor patrimonial líquido exceder a high-water mark. O montante real irá variar dependendo da performance do seu investimento. A estimativa de custo agregado acima inclui a média dos últimos 5 anos, ou desde a criação do produto, se for inferior a 5 anos.

- Custos de transação

- 0,84% O impacto dos custos inerentes às nossas operações de compra e de venda de investimentos subjacentes ao produto.

Desempenho anualizado

| Carmignac Portfolio Merger Arbitrage Plus | 3.2 |

| Carmignac Portfolio Merger Arbitrage Plus | - | - | + 4.3 % |

Fonte: Carmignac em 28 mar. 2024.

O desempenho passado não é necessariamente um indicador do desempenho futuro. Os desempenhos são líquidos de comissões (excluindo eventuais comissões de subscrição cobradas pelo distribuidor).

Insights mais recentes

Material de promoção. Este documento destina-se a clientes profissionais.

Comunicação promocional. Consulte o documento de informação fundamental/prospeto antes de tomar quaisquer decisões de investimento finais.

O presente material não pode ser total ou parcialmente reproduzido sem autorização prévia da Sociedade Gestora. O presente material não constitui qualquer oferta de subscrição nem consultoria de investimento. O presente material não se destina a fornecer consultoria contabilística, jurídica ou fiscal e não deve ser utilizado para estes efeitos. O presente material foi-lhe fornecido apenas para fins informativos e não o pode utilizar para avaliar as vantagens de investir em quaisquer títulos ou participações aqui referidas ou para quaisquer outros fins. As informações contidas neste material poderão ser apenas parciais e estão sujeitas a alterações sem aviso prévio. Estas informações são apresentadas à data em que foram escritas, derivam de fontes próprias e não próprias consideradas fiáveis pela Carmignac, não incluem necessariamente todos os pormenores e a sua precisão não é garantida. Como tal, não é dada qualquer garantia de precisão ou fiabilidade e a Carmignac, os seus diretores, colaboradores ou agentes não assumem qualquer responsabilidade decorrente de erros e omissões (incluindo a responsabilidade perante qualquer pessoa por motivo de negligência).

O desempenho passado não é necessariamente um indicador do desempenho futuro. Os desempenhos são líquidos de comissões (excluindo eventuais comissões de subscrição cobradas pelo distribuidor). No caso de ações sem cobertura cambial, o retorno poderá aumentar ou diminuir em resultado de flutuações cambiais. A referência a determinados títulos e instrumentos financeiros serve para fins ilustrativos para destacar ações incluídas, ou que já o tenham sido, em carteiras de fundos da gama Carmignac. Não se destina a promover o investimento direto nesses instrumentos, nem constitui consultoria de investimento. A Sociedade Gestora não está sujeita à proibição de negociação destes instrumentos antes de emitir qualquer comunicação. As carteiras dos fundos Carmignac estão sujeitas a alterações sem aviso prévio. A referência a uma classificação ou prémio não garante os futuros resultados do OIC ou do gestor.

Escala de Risco do KID (Documento de informação fundamental). O risco 1 não significa um investimento isento de risco. Este indicador pode variar ao longo do tempo. O horizonte de investimento recomendado é um mínimo e não uma recomendação de venda no final desse período.

Morningstar Rating™: © Morningstar, Inc. Todos os direitos reservados. As informações contidas neste documento: são propriedade da Morningstar e/ou dos seus fornecedores de conteúdos; não podem ser copiadas ou distribuídas; e não são garantidamente corretas, completas ou atempadas. Nem a Morningstar nem os seus fornecedores de conteúdos são responsáveis por quaisquer danos ou perdas decorrentes da utilização destas informações.

O acesso aos Fundos pode estar sujeito a restrições no que diz respeito a determinadas pessoas ou países. O presente material não é dirigido a nenhuma pessoa em qualquer jurisdição onde (em virtude da sua nacionalidade, residência ou outro motivo) o material ou a disponibilização deste material seja proibida. As pessoas sujeitas a tais proibições não deverão aceder a este material. A tributação depende da situação do indivíduo. Os Fundos não estão registados para distribuição a pequenos investidores na Ásia, no Japão, na América do Norte, nem estão registados na América do Sul. Os Fundos Carmignac estão registados em Singapura como um organismo estrangeiro restrito (apenas para clientes profissionais). Os Fundos não foram registados nos termos da US Securities Act de 1933. Os Fundos não podem ser oferecidos ou vendidos, direta ou indiretamente, por conta ou em nome de uma "Pessoa dos EUA", conforme definição dada no Regulamento S dos EUA e na FATCA. Os Fundos são registados junto da Comissão do Mercado de Valores Mobiliários (CMVM). A decisão de investir no fundo promovido deve ter em conta todas as características ou objetivos do fundo promovido, tal como descritos no respetivo prospeto. Os respetivos prospetos, KID e relatórios anuais do Fundo poderão ser encontrados em www.carmignac.com, www.fundinfo.com e www.morningstar.pt ou solicitados à Carmignac Gestion Luxembourg, Citylink, 7 rue de la Chapelle L-1325 Luxemburgo. Os riscos, comissões e despesas correntes encontram-se descritos no KID (Documento de informação fundamental). O KID deve ser disponibilizado ao subscritor antes da subscrição. O subscritor deverá ler o KID. Os investidores podem perder uma parte ou a totalidade do seu capital, pois o capital nos fundos não é garantido. Os Fundos apresentam um risco de perda do capital. Os investidores têm acesso a um resumo dos seus direitos no seguinte link: www.carmignac.pt/pt_PT/article-page/regulatory-information-6699

A Carmignac Portfolio refere-se aos subfundos da Carmignac Portfolio SICAV, uma sociedade de investimento de direito luxemburguês, em conformidade com a Diretiva OICVM.A Sociedade Gestora pode, a qualquer momento, cessar a promoção no seu país.Copyright: Os dados publicados nesta apresentação pertencem exclusivamente aos seus proprietários, tal como mencionado em cada página.